Fed Meeting: Is another Interest Rate Cut on the Horizon? What You Need to Know!

2025-03-19

Author: Kai

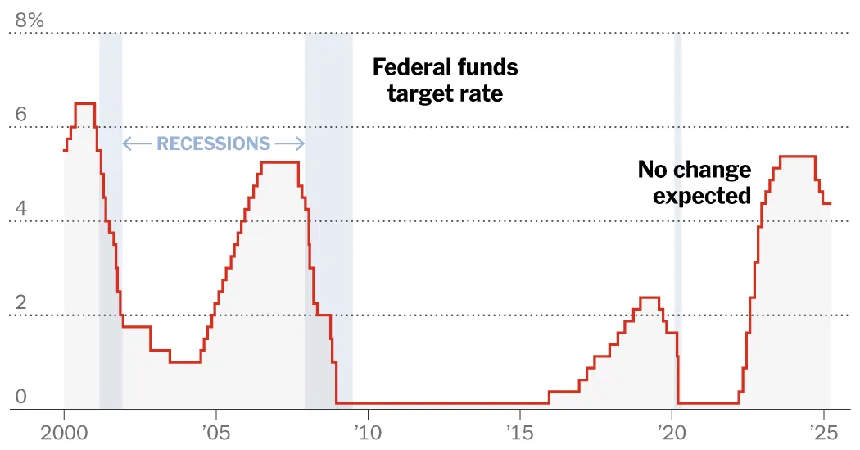

In a highly anticipated meeting, economists are not expecting the Federal Reserve to implement another interest rate cut anytime soon. This cautious approach comes amid an uncertain economic backdrop influenced by various factors, including President Trump's tariff policies, immigration issues, and significant federal job cuts that could reshape the landscape.

As it stands, the Fed's benchmark interest rate is between 4.25% and 4.5%. Over the past year, the central bank took decisive action against soaring inflation by rapidly increasing rates from near zero to above 5% between March 2022 and July 2023. Although inflation has begun to moderate, the Fed's recent moves towards cutting rates—with reductions occurring in September, November, and December—reflect a careful recalibration rather than an outright shift towards aggressive monetary easing.

Car Loans: The Affordability Challenge

Auto loan interest rates have seen an uptick, further complicating affordability as car prices continue to soar. The average rate for new car loans increased to 7.2% in February, up from 6.6% in December 2023 and significantly impacting borrowers’ ability to finance a vehicle. This trend is largely due to the influence of the five-year Treasury note yield, which ties closely with the Fed’s rates but is also affected by individual credit histories and broader market conditions. Notably, borrowers with lower credit scores face mounting challenges in securing favorable loan terms as delinquency rates rise.

Credit Card Rates: Slight Easing

On the credit card front, average interest rates have edged down slightly to 20.09% following the recent Fed cuts. However, much depends on individual credit scores and card types, with rewards cards often commanding higher rates. Research by the Consumer Financial Protection Bureau has found that the largest credit card issuers tend to charge rates that are significantly higher than smaller banks or credit unions—up to 10 percentage points more, which can result in an additional $400 to $500 in annual interest for average users.

Mortgage Market Dynamics

Mortgage rates have demonstrated volatility, peaking around 7.8% late last year before dropping to approximately 6.65% recently. Unlike other loan types, mortgage rates are primarily tethered to the yield on 10-year Treasury bonds. Home equity lines of credit and adjustable-rate mortgages are more immediately responsive to Fed rate decisions, making it imperative for prospective homeowners to shop around for the best rates and terms.

Savings Accounts: A Silver Lining?

As for savers, while the yield environment has changed little since the peak rates, online savings accounts are still delivering returns of 4% or more. Despite traditional banks lagging behind, the trend indicates that the market may provide opportunities for higher yields for those willing to explore.

Student Loans: The Time to Borrow?

Student loan interest rates vary, with fixed rates for federal loans set at 6.53% for undergraduates and up to 9.08% for PLUS loans. Federal loans typically offer more favorable terms compared to private loans, which are heavily influenced by the borrower's credit score. Consequently, extensive research is necessary for students and families to secure the best possible rates.

The Federal Reserve's Path Forward

The critical question looming over the economy is whether and when the Federal Reserve will resume rate cuts. When quarterly economic projections were last released, officials anticipated two quarter-point rate cuts throughout 2025, but recent developments indicate that Trump's policies might exert further inflationary pressures, complicating this outlook.

Economists are keenly observing the Fed’s "dot plot," which offers insight into officials' interest rate projections through 2027. The perceptions of inflation risks and economic growth remain paramount as the Fed navigates the complexities of maintaining a stable economy amidst external pressures.

The Impact of Tariffs and Economic Sentiment

As market confidence wavers, concerns over the potential consequences of Trump's tariff policies loom large. Analysts foresee the possibility of higher consumer prices, but the long-term inflation trajectory remains uncertain. Surprisingly, despite these fears, many experts do not predict an impending recession, citing the underlying strength of the American economy and its labor market.

Conclusion: What’s Next?

As we approach the Fed's upcoming meeting, all eyes are on how the central bank interprets the current economic landscape and what it may signal for future rate changes. While markets remain in a state of flux, the balance between stimulating growth and curbing inflation will challenge policymakers. This precarious dance means both businesses and consumers should prepare for a potentially turbulent economic forecast in the coming months.

Stay tuned for updates, as the Fed's decisions could have far-reaching implications for your finances!

Brasil (PT)

Brasil (PT)

Canada (EN)

Canada (EN)

Chile (ES)

Chile (ES)

Česko (CS)

Česko (CS)

대한민국 (KO)

대한민국 (KO)

España (ES)

España (ES)

France (FR)

France (FR)

Hong Kong (EN)

Hong Kong (EN)

Italia (IT)

Italia (IT)

日本 (JA)

日本 (JA)

Magyarország (HU)

Magyarország (HU)

Norge (NO)

Norge (NO)

Polska (PL)

Polska (PL)

Schweiz (DE)

Schweiz (DE)

Singapore (EN)

Singapore (EN)

Sverige (SV)

Sverige (SV)

Suomi (FI)

Suomi (FI)

Türkiye (TR)

Türkiye (TR)

الإمارات العربية المتحدة (AR)

الإمارات العربية المتحدة (AR)